Many people are familiar with the concept of a 401(k), but fewer know about the HSA, or Health Savings Account. This investment account is actually a gem that can provide many benefits, especially if you are self-employed.

One of the biggest advantages of an HSA is that it allows you to set aside money for healthcare expenses tax-free. This means that you can use the money in your account to pay for deductibles, copays, and other qualifying medical expenses without having to pay any taxes on the withdrawals. In addition, the money in your HSA can be invested and allowed to grow tax-deferred.

This means that you can potentially enjoy a larger return on your investment than you would with a traditional savings account.

Lastly, HSAs are portable, which means that you can take them with you if you change jobs or retire. With all of these advantages, it’s no wonder that more and more people are opening HSAs each year.

What is an HSA and how does it work?

Health Savings Accounts, or HSAs, are a type of savings account that can be used to pay for medical expenses. Anyone who is enrolled in a high-deductible health plan is eligible to open an HSA. Contributions to an HSA are tax-deductible, and the money in the account grows tax-free.

Withdrawals from an HSA are also tax-free, as long as they are used to pay for qualified medical expenses. Because of the tax benefits, HSAs can be a great way to save for medical expenses in the short-term and the long-term.

Additionally, some employers will make contributions to their employees’ HSAs, making them an even more valuable benefit. If you are eligible for an HSA, it can be a great way to save for your medical needs.

The benefits of using an HSA

One of the biggest benefits of an HSA is that it can help you save on your taxes. Here are some points to keep in mind:

- Since the money in your HSA is contributed on a pre-tax basis, you can reduce your taxable income by contributing to an HSA.

- Additionally, any interest or investment earnings on the money in your HSA are tax-free. And finally, withdrawals from your HSA are also tax-free as long as they are used to pay for qualified medical expenses.

- Another benefit of an HSA is that it can help you cover unexpected medical expenses. Unlike a traditional health insurance plan, which has a deductible that you must meet before coverage kicks in, an HSA allows you to start using your account immediately to pay for eligible medical expenses. This can be especially helpful if you have a high-deductible health insurance plan.

- Lastly, an HSA can act as a retirement account for healthcare expenses. Unlike other retirement accounts, such as a 401(k) or IRA, there are no taxes due on withdrawals from your HSA as long as they are used to pay for qualified medical expenses. This makes an HSA a great way to save for future healthcare costs in retirement.

How to maximize your contributions to your HAS

If your employer offers to contribute to your HSA, make sure you take advantage of that! The amount they contribute can vary, but it’s always helpful to have the extra money in your account to cover unexpected healthcare costs. Even if your employer only contributes a small amount, it’s still worth taking advantage of their offer.

Invest in an HSA-eligible health plan

To be eligible for an HSA, you must have a qualified High Deductible Health Plan (HDHP). This type of plan typically has lower monthly premiums than other health plans, which can help you save money in the long run.

It’s important to shop around and compare different HDHPs before enrolling in one so that you can find the best plan for your needs and budget.

Invest Your HSA Contributions Wisely

Once you have money in your HSA, it’s important to invest it wisely so that you can grow your account balance and cover future healthcare costs. There are a few different ways to do this, but one option is to invest in a Health Savings Investment Account (HSIA).

This type of account allows you to invest your HSA funds in a variety of investment vehicles, such as stocks or mutual funds.

Another option is to use a health savings debit card, which allows you to pay for eligible healthcare expenses directly from your HSA without having to worry about reimbursement later on.

Use Your HSA Funds Before They Expire

One of the great things about an HSA is that the funds roll over from year to year, so you don’t have to worry about them expiring like with other types of health insurance plans.

However, this doesn’t mean that you should let your HSA balance build up and never use it! Be sure to use your HSA funds as needed so that you can get the most out of them.

For example, if you know you’re going to need a major dental procedure next year, start setting aside money in your HSA now so that you can cover the cost when the time comes.

Examples of ways to use your HSA funds

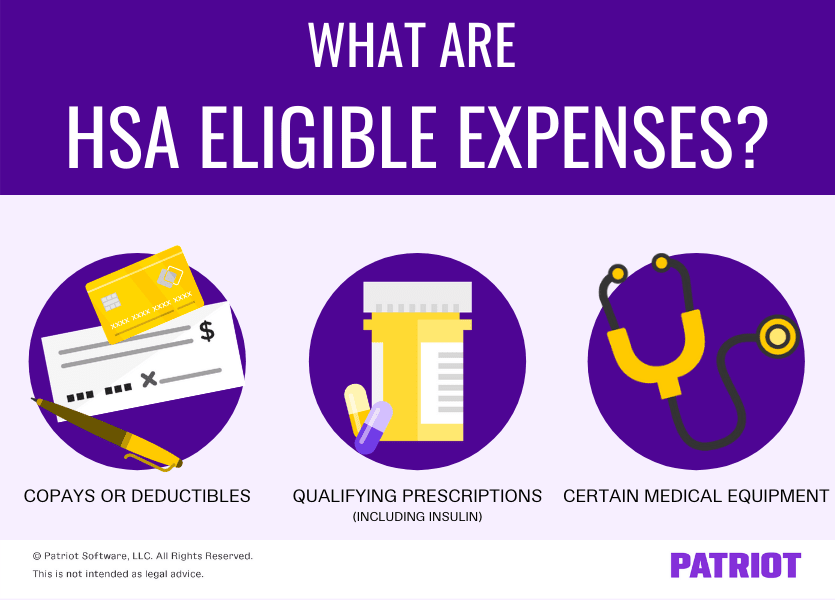

One of the great things about an HSA is that it can be used to cover a wide range of eligible medical expenses. These include everything from doctor visits and prescription medications to dental care and vision care. You can also use your HSA to pay for health insurance premiums, as well as long-term care insurance premiums.

Tax advantages

Another big advantage of an HSA is that the funds you contribute are tax-deductible. Additionally, the earnings on your account are tax-free, and withdrawals for eligible medical expenses are also tax-free. This makes an HSA a great way to save for future medical expenses in a tax-advantaged way.

Save for retirement

In addition to using your HSA to cover current medical expenses, you can also let the funds grow over time and use them to pay for medical expenses in retirement. Since the money in your HSA is tax-free, this can be a great way to stretch your retirement savings further.

Use it like a savings account

While an HSA is technically a health insurance product, you can also use it like a savings account to cover unexpected medical expenses. For example, if you have a high deductible health plan, you can use your HSA funds to cover your deductible if you need to go to the hospital or have major surgery.

Conclusion

An HSA is a great way to save for healthcare expenses – both current and future. And because contributions are tax-deductible and earnings are tax-free, an HSA can also be used as an investment account. If you’re not already taking advantage of an HSA, now is the time to start contributing!